When the Paycheck Stops: My Real Talk on Staying Afloat After Job Loss

Losing your job hits like a storm—you see it coming, but you’re never ready. I’ve been there, staring at bills with no income in sight. That’s when timing isn’t just important—it’s everything. What you do in the first days, weeks, and months can make or break your financial recovery. This isn’t theory; it’s what I lived through, tested, and reshaped into a plan that actually works. It’s not about getting rich quick or chasing miracles. It’s about staying grounded, making clear decisions, and protecting your future when the ground beneath you feels like it’s shifting. The paycheck may stop, but your control doesn’t have to.

The Moment It Happens: What to Do in the First 48 Hours

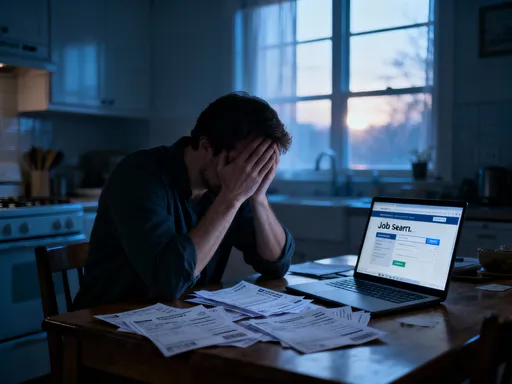

When the news comes, whether expected or sudden, the emotional weight is immense. The mind races: How will the mortgage be paid? What about the kids’ tuition? Can we keep the car? In those first 48 hours, fear can easily override logic. But this initial window is not for despair—it’s for decisive, calm action. The goal is not to solve everything but to stabilize. The first step is to pause. Not in the sense of doing nothing, but in halting non-essential spending immediately. That subscription box, the weekly takeout, the gym membership you haven’t used in months—these are not luxuries now, they are liabilities. Freeze them. Cancel them. Redirect every possible dollar toward essentials.

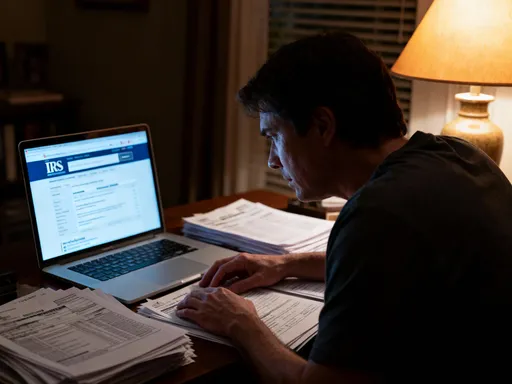

Simultaneously, confirm your eligibility for unemployment benefits. In many countries, including the United States, these benefits are designed to act as a temporary income bridge. Yet too many people delay filing due to pride, confusion, or misinformation. The truth is, unemployment insurance is not charity—it’s a benefit you paid into through years of employment. Delaying your claim means losing weeks of support you’re entitled to. Gather your documents: employment history, company name, dates of service, reason for separation. Submit the application online the same day you receive notice, if possible. Set calendar reminders for weekly check-ins, as most systems require active confirmation of job search efforts to continue receiving funds.

Next, assess your emergency fund. If you have one, this is its moment. But resist the urge to drain it all at once. Instead, calculate your monthly essential expenses—housing, utilities, groceries, transportation, minimum debt payments—and divide your available savings by that number. This gives you a realistic runway. Knowing how many months you can cover brings clarity and reduces panic. If you don’t have an emergency fund, don’t spiral. Focus on what you *can* control: cutting costs, accessing benefits, and preparing for income alternatives. The key is to act with purpose, not emotion. Every decision made in these first two days sets a precedent. Will you react in fear or respond with strategy? The answer shapes everything that follows.

Why Timing Trumps Everything in Financial Survival

Speed matters, but sequence matters more. Acting quickly without a plan can do more harm than good. Imagine withdrawing from your retirement account before filing for unemployment. You might trigger a tax event, reduce long-term security, and still not cover six months of expenses. That’s why timing isn’t just about being fast—it’s about being smart. Each financial decision during unemployment has a ripple effect. Delay filing for benefits by two weeks? That’s two weeks of lost income. Wait a month to contact your lender about mortgage forbearance? You may already be reported as delinquent, damaging your credit score.

Consider healthcare. Losing employer-sponsored insurance is one of the most stressful aspects of job loss. Yet many wait too long to explore options, risking coverage gaps that could lead to massive bills if an emergency arises. The moment you lose your job, you gain access to COBRA, which allows you to continue your current plan at your own expense, or you can enroll in a marketplace plan through government exchanges. There’s a special enrollment period for exactly this life event. Waiting even a few weeks could leave you uninsured during a critical time. The same principle applies to credit cards. If you anticipate missing a payment, call the issuer *before* the due date. Many offer hardship programs that reduce interest, waive fees, or allow temporary pauses. But these programs require proactive communication. Once you’re late, your options shrink.

Timing also affects job search momentum. The longer you wait to update your resume, reach out to contacts, or apply for roles, the more stagnant your prospects become. Employers often favor candidates with recent activity. A gap in employment is harder to explain than a period of active transition. The first month after job loss should be treated as a full-time job in itself—one focused on stabilization and preparation. Every action, from applying for benefits to scheduling skill-building webinars, compounds over time. A delay of a week here, a missed deadline there, may seem small, but together they erode your financial and emotional resilience. Precision in timing isn—not just urgency—is what separates survival from setback.

Building Your Financial Firewall: Protecting What’s Left

When income stops, the priority shifts from growth to preservation. Think of your remaining resources as a fortress under siege. Your goal isn’t to expand the walls but to reinforce them. This is where a financial firewall comes in—a structured approach to shielding your core assets from unnecessary erosion. The first step is to categorize every expense as essential or optional. Essentials include rent or mortgage, utilities, groceries, transportation to job interviews, and minimum debt payments. Everything else—entertainment, dining out, travel, non-critical subscriptions—falls into the optional bucket. Be ruthless. This isn’t permanent austerity; it’s temporary triage.

Once you’ve mapped your spending, renegotiate what you can. Many people don’t realize that bills aren’t set in stone. Call your internet provider and ask for a retention discount. Switch to a cheaper cell phone plan. Request a reduction in your car insurance premium by adjusting coverage or increasing your deductible temporarily. Some utility companies offer budget billing, which spreads annual costs into predictable monthly payments. Even your landlord may be willing to pause a rent increase or offer a short-term deferral if you communicate openly and respectfully. The key is to initiate the conversation early, before you miss a payment. Lenders and service providers are more likely to help when they see responsibility, not crisis.

Your emergency fund is part of this firewall, but it must be managed wisely. Withdraw only what you need, when you need it. Avoid dipping into retirement accounts like 401(k)s or IRAs unless absolutely necessary. Early withdrawals often come with a 10% penalty, plus income taxes, turning a $10,000 withdrawal into roughly $7,000 after deductions. More importantly, you lose the power of compound growth. That money isn’t just gone—it’s the future security of your retirement. Instead, explore alternatives: selling unused items, taking on short-term work, or borrowing from family with a clear repayment plan. If you must use retirement funds, consider a loan first, if your plan allows it, as it avoids taxes and penalties as long as you repay it.

A strong firewall also includes knowing your rights. In many regions, there are protections against utility shutoffs, eviction moratoriums, or mortgage forbearance options. These aren’t handouts—they’re safeguards built into the system for times like this. Ignorance of them leaves you vulnerable. Take time to research local resources: food banks, community assistance programs, career counseling services. These aren’t signs of failure—they’re tools of resilience. Protecting what’s left isn’t about fear. It’s about respect for the effort it took to earn it and the future it’s meant to support.

Income Gaps Don’t Last Forever—But Mistakes Do

Unemployment is a season, not a sentence. Most people return to work within months, especially when they take proactive steps. But the choices made during this gap can echo for years. The temptation is to grab any source of quick cash, but not all income is created equal. Some options offer immediate relief at long-term cost. High-fee gig apps, for example, may promise flexibility, but after platform cuts, fuel, and vehicle wear, the net gain can be minimal. Payday loans or cash advances might cover a bill today but lead to a cycle of debt with interest rates exceeding 300%. These are quick fixes that deepen the hole.

Better alternatives exist. Skilled freelancing—writing, bookkeeping, graphic design, virtual assistance—allows you to leverage existing talents for sustainable income. Platforms like Upwork or Fiverr connect freelancers with clients worldwide, often at rates far above minimum wage. Even a few hours a week can cover groceries or a utility bill. Part-time contract work in retail, customer service, or administrative support offers stability and sometimes benefits. Some companies hire contract workers with the possibility of full-time conversion. Monetizing underused assets is another smart path. Renting out a spare room through regulated platforms, selling quality clothing or electronics, or offering tutoring or consulting services turns idle resources into cash flow.

The key is to align short-term income with long-term goals. A job that pays slightly less but offers flexibility to attend interviews or upskill may be more valuable than one that drains your time and energy. Consider bartering: offering services in exchange for goods or help with errands. Community networks often thrive on this kind of mutual support. Every dollar earned during unemployment isn’t just income—it’s a signal of capability, a boost to confidence, and a reduction in the pressure to make desperate financial choices. Small, smart moves compound. A $200 freelance project this week, another next month, builds momentum. It proves you’re not passive. You’re adapting. And that mindset is as crucial as the money itself.

When to Reinvest—And When to Hold Back

Even without a paycheck, your investments still exist. And how you manage them during unemployment can significantly impact your long-term financial health. The instinct during crisis is often to sell—to convert stocks or mutual funds into cash for immediate use. But panic-selling locks in losses and undermines years of growth. Markets fluctuate; downturns are normal. Selling at a low means you miss the recovery. History shows that staying invested through volatility typically yields better returns than trying to time the market.

Instead of reacting, assess. Review your portfolio not to make changes, but to understand risk exposure. Are your investments too aggressive for your current situation? If a large portion is in high-growth stocks, consider rebalancing slightly toward more stable assets like bonds or dividend-paying funds. This isn’t about abandoning growth, but about reducing volatility when you can’t afford big swings. At the same time, pause new contributions to retirement accounts if necessary. It’s okay to hit pause. The goal isn’t to grow wealth now, but to preserve it.

One powerful concept is the idea of “mental accounts.” Treat your emergency fund as completely separate from your investment portfolio. The first is for survival, the second for the future. Blurring the lines leads to poor decisions. Just because you have $50,000 in investments doesn’t mean you should liquidate it to cover three months of rent. That money has a different purpose. Use it only if all other options are exhausted and the need is critical. Consider consulting a fee-only financial advisor for an objective review. Many offer sliding scale fees or pro bono services during hardship. Clarity, not action, is the goal here. You don’t need to do everything at once. You need to avoid irreversible mistakes.

The Hidden Costs of Waiting Too Long

Procrastination is expensive. The longer you wait to address financial realities, the higher the cost. Delaying communication with creditors can lead to late fees, penalty interest, and credit score damage. A single missed payment can drop your score by 100 points or more, affecting future loan approvals and interest rates for years. Health coverage gaps can result in tens of thousands in medical bills from a single emergency. Skipping skill development or networking delays reemployment, extending the income gap.

Many avoid these conversations out of shame or fear. But silence helps no one. Lenders would rather work with someone who communicates than someone who disappears. Most have hardship programs designed to prevent default. The same goes for utility companies, landlords, and service providers. The moment you know you’ll miss a payment, reach out. Explain your situation honestly. Ask what options exist. Most will respond better to a proactive call than a late notice.

Ignoring personal development is another hidden cost. The job market evolves quickly. Skills that were in demand five years ago may be obsolete today. Waiting to update your resume, learn new software, or earn a certification puts you behind. But even 30 minutes a day of online learning adds up. Free or low-cost platforms like Coursera, LinkedIn Learning, or Khan Academy offer courses in high-demand fields. Completing one can boost your resume and confidence. Networking is equally important. Reach out to former colleagues, join industry groups, attend virtual events. Opportunities often come through people, not job boards. Every day you wait to take these steps, you lose ground. But every small action builds momentum. The cost of waiting isn’t just financial—it’s emotional and professional. Taking control, even in small ways, restores dignity and direction.

From Survival to Strategy: Planning the Comeback

Recovery begins before the next job offer arrives. While managing cash flow is essential, true financial healing requires forward motion. This is the shift from survival mode to strategic rebuilding. Update your resume with recent accomplishments and skills. Tailor it for the roles you’re targeting, using keywords from job descriptions to pass automated screening systems. Write a strong cover letter that tells your story—not just your experience, but your resilience, adaptability, and commitment.

Expand your network intentionally. Contact former coworkers, managers, mentors. Let them know you’re looking and what kind of role you want. Many jobs are filled through referrals before they’re even posted. Attend virtual career fairs, join professional associations, participate in online forums. Every connection increases your visibility. At the same time, align your job search with market demand. Research growing industries in your area or those open to remote work. Consider transferable skills. A teacher’s communication and organization skills are valuable in corporate training. A retail manager’s leadership experience applies to operations roles. Reframing your background makes you more competitive.

Financial healing and career rebuilding are not separate processes—they are intertwined. Every step toward reemployment reduces financial pressure. Every financial decision made with care preserves your future. The comeback isn’t just about landing a job. It’s about returning stronger, wiser, and more resilient. The storm of job loss doesn’t define you. What defines you is how you respond. By acting early, protecting your resources, avoiding costly mistakes, and preparing for the next chapter, you turn crisis into transformation. Timing, discipline, and resilience—these are not just strategies. They are the foundation of lasting financial well-being.